Since 1980, The Church Pension Fund (CPF) has made a defined benefit plan for lay employees, The Episcopal Church Lay Employees’ Retirement Plan (Lay DB Plan), available to Episcopal employers who choose to participate. Since the 1990s, CPF has also made a defined contribution plan, similar to a 401(k) plan, available to employers with lay employees. Over the decades, the General Convention has passed resolutions urging employers to provide lay pension benefits. Some employers complied, but too many others did not.

In 2006, at the request of the Executive Council, the General Convention passed Resolution 2006-A125, which authorized the Office of Ministry Development to “take the lead on determining the best way to conduct a feasibility study examining whether pension benefits for lay employees should be made compulsory and be administered by a single provider,” as was the case for clergy.

CPG played a critical role in the feasibility study, providing data on lay employee demographics, compensation, and benefits per Resolution 2006-A125. At the conclusion of this work, which was collaborative and exhaustive, the Executive Council put forward Resolution 2009-A138. Resolution 2009-A138 amended Canon 8 of the Episcopal Church Canons to make lay pensions mandatory, established eligibility requirements for participation, named CPF as administrator of a Lay Employee Pension System (LPS), gave employers flexibility to choose a defined contribution or defined benefit pension plan for their lay employees, and set contribution minimums for participating employers.

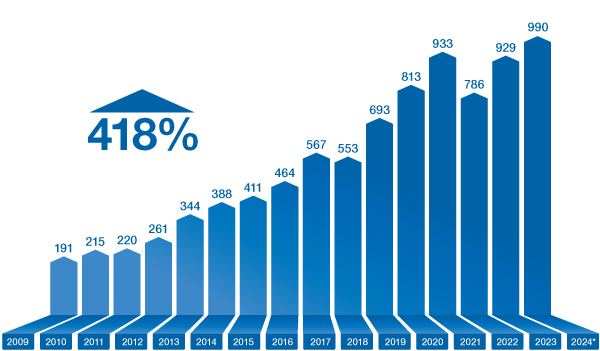

Enrollment in the LPS has been strong; all dioceses in the United States offer eligible lay employees at least one of the retirement plans. The overwhelming majority of employers (89%) offer The Episcopal Church Lay Employees’ Defined Contribution Retirement Plan (Lay DC Plan); approximately 94% of the eligible lay employees reported to CPG are enrolled. A much smaller number of employers and employees participate in the Lay DB Plan. CPG’s role has been to administer both plans and encourage individuals to save through ongoing education and outreach. Since 2009, there has been a 148%* increase in lay employee retirement savings accounts, and assets held in these accounts have grown 418%* due to increased contributions and strong market returns and currently stand at more than $1 billion. The LPS has been effective at improving the retirement outlook for eligible lay employees.

Periodically, we survey lay employees to gauge their confidence in retirement savings. Our last survey revealed that lay employees were happy with their retirement savings options but didn’t feel completely confident that they’d have sufficient assets to retire. There is more work to do, and we are exploring new, additional ways to encourage lay employees and their employers to increase contribution levels when funds are available. We constantly remind clients that Resolution 2009-A138 established minimum contribution amounts, but employers and employees are allowed to do more, and some do.

While lay employee pension benefits are competitive and have been well received and well utilized, they are not identical to clergy pension benefits. This reality has caused tension for some in the Church, and CPG has found itself in the middle of a discussion that only the Church can fully address.

All eligible clergy in The Episcopal Church participate in a 107-year-old, mandatory defined benefit plan. For more than a century, Episcopal employers have been required to pay an assessment equal to a fixed percentage (currently 18%) of a clergyperson’s compensation to CPF, and CPF has invested those assets well. As a result, The Church Pension Fund Clergy Pension Plan (Clergy Pension Plan) has matured into a strong, well-funded plan that can afford a bundle of benefits for clergy that exceeds the value of benefits available to lay employees who participate in the much smaller and newer Lay DB Plan that has a maximum mandated contribution of 9% of compensation.

We have been asked what would be necessary to achieve parity in retirement benefits between clergy and lay employees. Assuming clergy benefits remain unchanged, at a minimum, the Church would have to mandate that all lay employees participate in the Lay DB Plan (rather than only in defined contribution plans) and that the assessment rate be raised from the current 9% to 18%. Even then, it would take many years for the assets of the Lay DB Plan to grow sufficiently to afford the full menu of benefits available to clergy who participate in the Clergy Pension Plan. It should be noted that applicable law prevents CPF from using assets in the Clergy Pension Plan to subsidize lay pension benefits. The Church, not CPF, would have to source additional funds for lay pensions.

In the meantime, CPG continues to do its very best with the resources entrusted to us to help lay employees prepare for retirement and to help the Church understand the state of pension parity, including actions that could be taken to create greater parity. We have issued two comprehensive reports (Resolution 2018-D045: Study Equity in Clergy and Lay Pension Plans and Resolution 2018-A237: Study Parity Between Lay and Clergy Pensions) at the urging of the General Convention, and we commend them to the Church still.

* As of 3/31/24